Administrative discharge, or statutory discharge, is a potential way to discharge your federal student loans without the need for a bankruptcy. The administrative discharge provisions are mostly unknown to individuals with student debt, so you need a student loan lawyer to help analyze your situation and make sure that all requirements are met should you qualify for an administrative discharge.

This type of discharge is a great way to get rid of your remaining student loan debt you’re your acceptance into one of the available programs. Some of the provisions of administrative discharges are easier to prove than others, but all require the correct procedures and paperwork in filing.

Surprisingly, the US Department of Education is not required to notify student loan borrowers of their potential for discharging student debt through an administrative discharge! This is where an experienced federal student loan lawyer can help. We will analyze your situation to determine which administrative discharge may apply to you and ensure that all the required materials are provided to the right people.

What administrative discharge programs are available for federal student loans?

Administrative discharge programs are relatively unknown to the people that can use them. With that being said, there are a number of administrative discharge programs available for federal student loans. These programs differ greatly in the requirements and necessary paperwork, but they can all lead to the same end, namely discharge of the remaining balance of your student debt.

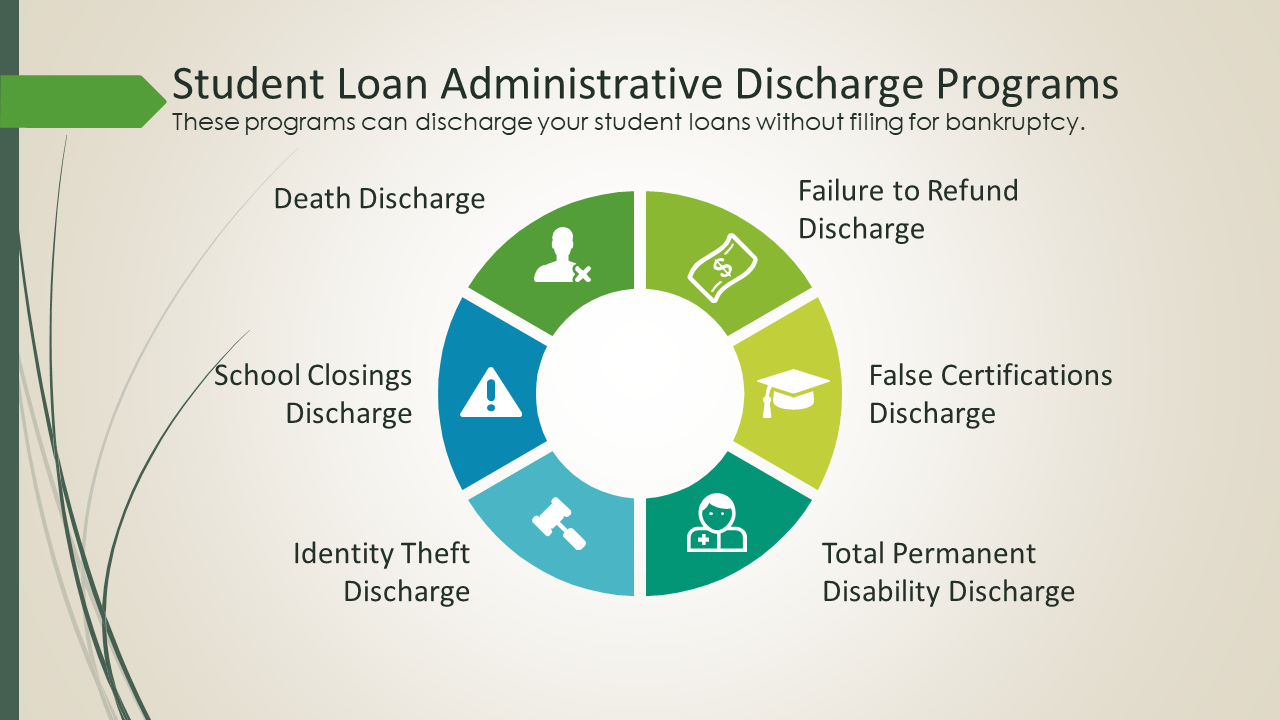

The administrative discharge programs available to federal student loan borrowers include:

- Death Discharge

- School Closings Discharge

- Identity Theft Discharge

- Failure to Refund Discharge

- False Certifications/Defense to Repayment Discharge

- Total Permanent Disability Discharge

We’ll go into more details for these administrative discharge programs below.

Death Discharge

In the event that an individual with a federal student loan passes away, the loan will be discharged. This is not much help to the person passing away; however, if you are a parent of a student who had a Parent PLUS loan, you may also qualify for death discharge should the student pass away.

The procedure for applying for a death discharge is relatively straightforward and simple, but the necessary documents must be correctly attached to the application, so it is important to understand the application. It is also important to note that the US Department of Education will generally not attempt to collect a student debt balance from an estate.

School Closings Discharge

If a school an individual is enrolled at closes during the time said individual is enrolled there or very soon thereafter, the individual may be able to secure a discharge of the remaining amount of his/her student debt incurred while attending said school. This type of discharge has become important because it helps in dealing with schools that potentially start up simply for the purpose of taking money from students and closing soon after. It is important to note that this discharge does not apply to schools that only lose an accreditation and do not actually close.

One problem individuals face in applying for this discharge is that there are tight deadlines. Additionally, the student must be unable to complete his/her education, meaning they cannot receive this discharge if they graduate or if the credits obtained from the closed school are transferable to another institution. Furthermore, damage to reputation of the degree obtained based on the school closing is not a cause to have your loan discharged.

An experienced student loan lawyer can be especially helpful in regard to this type of administrative discharge because it can require sworn statements from the student, proof that there is no way to complete the coursework or get credit for the completed classes elsewhere and information relating to other loans or benefits received.

Identity Theft Discharge

The identity theft discharge is fairly straightforward and requires a showing that an individual was the victim of identity theft or a similar wrong in regard to a student loan. For the purpose of this discharge, identity theft usually relates to the forging of the individual’s signature on a student loan application, thereby applying for the loan in said individuals name.

If a discharge is secured based on identity theft, the individual can recover any past payments and avoid having to make any future payments on the student loan. It may sound simple enough to prove that you were the victim of identity theft; however, it is important to note that simply stating that you were a victim of identity theft is not enough, strict proof of this type of crime is required.

Failure to Refund Discharge

This type of discharge involves either a school closing or a student withdrawing from a school. In a situation where either of these things occurs, the school will generally be responsible for partially refunding any unused or unearned student loans proceeds. If the school fails to refund the correct amount, the student can then seek a discharge of the loan amount that should have been refunded. However, student loan borrowers must first seek to recover the refund from the school before attempting to discharge the amount.

False Certifications/Defense to Repayment Discharge

Have you been taken advantage of by a school that falsely certified your ability to benefit from attending the school or falsely certified that you meet the eligibility requirements for a student loan? Were you misled about the requirements for employment in the occupation for which the training program was intended? If yes, then this is a discharge option for you.

The false certifications/defense to repayment discharge encompasses many different scenarios with some be fairly simple to prove such as a showing that you did not have a high school diploma or GED. On the other hand, some cases require a great deal of story telling that an experienced student loan lawyer will be best able to put together. These cases can require a showing of proof that you were misled, there was some type of fraud, or there were material misrepresentations that caused you to enroll in the school.

Most of the more complex cases will require you to show that had the truth been conveyed, you would not have enrolled and the student loans would not have been disbursed. Some documents that can help are advertisements, enrollment materials, or stories from other classmates that are like your experience. An experience student loan attorney can strongly improve your chances in this discharge option because it is all about putting together a story that will show how you were harmed by what the school promised you.

Total Permanent Disability Discharge (TPD Discharge)

If you are totally and permanently disabled, you may qualify for a total and permanent disability discharge (TPD discharge)of your federal student loans or TEACH Grant service obligation. This is a common type of administrative discharge.

A TPD discharge relieves you from having to repay a William D. Ford Federal Direct Loan (Direct Loan) Program loan, Federal Family Education Loan (FFEL) Program loan, and/or Federal Perkins Loan (Perkins Loan) Program loan or complete a TEACH Grant service obligation on the basis of your total and permanent disability.

This is where a federal student loan lawyer can help. You need to submit the right documentation to prove you’re disabled and that you met the qualification of the program. We have a unique perspective in addressing a TPD discharge because we are not only student loan lawyers, but also Social Security disability lawyers. We can help you prove you are disabled.

We explain the details of the total and permanent disability discharge here.

How can a lawyer help with administrative discharge of student loans?

The most important way our student loan lawyers can help with your potential administrative discharge is to put together your application including the required information and documents. No matter how easy some of the programs may seem to you, the application process can be daunting and must be done correctly to secure your discharge.

Additionally, as we discussed above, many people do not know about the different administrative discharge options and you can count on the fact that the US Department of Education will not be jumping at the chance to help you. So, we are here to analyze your specific situation and make sure that you are given the best option, whether that be administrative discharge or not, to get rid of or limit your student debt.

Every case is different and a student loan lawyer can give you advice specific to your situation.

Does an administrative discharge of student loans require bankruptcy?

No. The administrative discharge programs generally require the completion of an application and including all of the necessary documentation. Unlike other types of discharge options that may require you to file for bankruptcy, this option does not.

Contact an administrative discharge lawyer today

The administrative discharge options offered for federal student loans can be a great way to get rid of some or all of your student debt, especially in cases where a school has essentially lied to you about its program. ARM Lawyers can skillfully guide you through the process and in choosing the best option for your specific situation. Call or e-mail us today.