A consumer law attorney can help you enforce your rights. Whether this involves unfair debt collection practices, inaccurate credit reporting, or resolving student loan issues, consumers face potential harms in every transaction. An experienced consumer lawyer can help you protect yourself against these predatory industries and give you the comfort you deserve. As your consumer lawyers, we fight for you – not for the major corporations.

What is consumer law?

Consumer law is the general term applied to a category of law designed to protect consumers. These laws include federal laws and state laws that prevent people from being taken advantage of by lenders, dealers, debt collectors, or other small and large businesses. Many of these consumer protection laws allow for individuals to sue if they’ve been harmed but also allow the federal or state government to enforce the laws criminally and civilly.

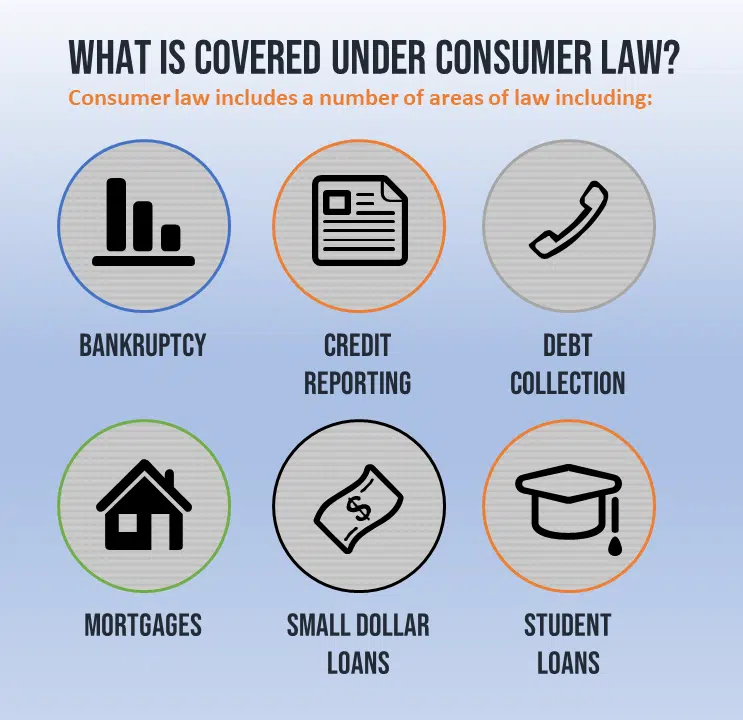

What is covered under consumer law?

Consumer law includes a number of areas of law including:

- Bankruptcy – The liquidation (Chapter 7) or reorganization (Chapter 13) of debts.

- Credit Reporting – Credit errors, identity theft, privacy invasion, and other violations of the Fair Credit Reporting Act (FCRA).

- Fair Debt Collection Practices – Defense against unfair, abusive, or unwarranted debt collection practices including improper garnishment actions. This includes debt collector harassment.

- Mortgages – Scams or unfair practices related to the sale or financing of a mortgage, home improvement or repairs, foreclosure defense, landlord and tenant issues, mobile or manufactured homes, and timeshares.

- Small Dollar Loans – Unfair small dollar loans including payday, car titles, or tax refund loans.

Consumer law in Pennsylvania

Pennsylvania has a number of consumer protection laws in place to protect its citizens. Pennsylvania citizens not only get the protection of federal laws such as the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA), but also get the additional protection of the Fair Credit Extension Uniformity Act (FCEUA) and the Unfair Trade Practices Act and Consumer Protection Law (UTPCPL). In many cases, it is possible for a consumer to sue under both the federal and Pennsylvania laws.

The FCEUA regulates the debt collection activities of debt collectors and creditors in Pennsylvania. This law prohibits debt collectors and creditors from engaging in certain unfair or deceptive acts or practices while attempting to collect debts. The FCEUA Act encompasses the federal debt collection statute, the FDCPA, and provides certain important restrictions on the conduct of debt collectors.

Pennsylvania also has a number of laws protecting mortgage borrowers. In addition to the federal Real Estate Settlement Procedures Act of 1974 (RESPA), Pennsylvania also protects borrowers through Act 6 and Act 91. When the collateral is owner-occupied residential property Pennsylvania Act 91 limits the lender’s right to accelerate the debt, affords the borrower a right to cure defaults, requires the lender to notify the borrower of that right and of the right to seek mortgage assistance, and stays foreclosure proceedings while the borrower seeks assistance.

Even when the property is not owner-occupied, Pennsylvania Act 6 may require the lender to jump through more hoops before it can foreclose. Among other things, Act 6 requires the holder of a “residential mortgage” to give the borrower notice of default before accelerating the debt, limits the rate of interest that may be charged, limits the attorneys’ fees that may be charged to the borrower, and prohibits the lender from foreclosing by executing on a judgment by confession unless it has first obtained a judgment of foreclosure in a “conforming action.”

What does a consumer law attorney do?

Consumer lawyers represent people who have been victimized by fraudulent, abusive, and predatory business practices. In many cases, this involves suing the business that violated the consumers rights. Whether that business engaged in unfair debt collection practices, inaccurate credit reporting, or other abusive conduct, a consumer law attorney can sue to protect your rights. Many consumer protection laws allow a consumer lawyer to sue for any harm done to you as well as attorneys’ fees. This allows you to be made whole by the lawsuit without having to pay out of pocket.

Do I need a consumer lawyer?

Often times it is difficult to file a lawsuit against a major corporation without the assistance of a consumer lawyer. These companies are often multi-billion dollar industries and have lawyers prepared to defend them for even the most abusive conduct. Without a consumer law attorney who is familiar with the law and court procedures, it is possible to lose your case.

Because consumer lawyers generally charge contingency fees and because most consumer protection laws allow you to recover attorneys’ fees, there is little downside to hiring a consumer law attorney to assist you.

How much do consumer law attorneys charge?

There is no uniform fee structure amongst consumer lawyers, but most charge contingency fees. This means that there is no money due up front and no money due unless you recover money from the other party. Many of the consumer protection laws we use allow us to recover attorneys’ fees from the other party. That means that generally you will not be responsible for paying the lawyer directly. For example, if a debt collector engages in abusive conduct, they may be required to pay you for their violations of the law, but would also be required to pay the lawyer who helped you sue.

Consumer law attorney in Pennsylvania

Take back control of your life and your rights. Providing both immediate relief and long-term solutions, our attorneys could be the answer you have been looking for. Our Pennsylvania consumer lawyer strives to make this process as easy as possible. Contact our law office today to schedule a free consumer law consultation!

- Stroudsburg consumer law attorney

- Palmerton consumer law attorney

- Bethlehem consumer law attorney

- Pittston consumer law attorney

- Cranberry Township consumer law attorney

The best part is that we can start the whole process over the phone or by video conference so you don’t even need to come into the office! We make everything as easy as possible for you from start to finish. Call us today.