Your first step in your bankruptcy journey with our office is your free bankruptcy consultation. In this meeting, we will get the necessary information we need in order to give you the best possible advice. We’ll start by determining if bankruptcy is right for you. Bankruptcy is a very powerful financial tool and can help people in many situations, but it cannot fix everything. Sometimes, we may recommend non-bankruptcy solutions.

If we determine that bankruptcy is right for you, we will recommend what bankruptcy chapter is best for you. When most people think of bankruptcy, they think of Chapter 7, but Chapter 7 bankruptcy is not right for everyone. Some people will actually pay less in a Chapter 13 bankruptcy! We will go over this during your free bankruptcy consultation so you understand exactly why we are giving you the advice we are giving you.

We do offer free bankruptcy consultations by phone or video chat to make it easier for our clients. Just let us know what you’d prefer.

If you haven’t scheduled your free bankruptcy consultation yet, just call us!

How to Prepare for Your Free Bankruptcy Consultation

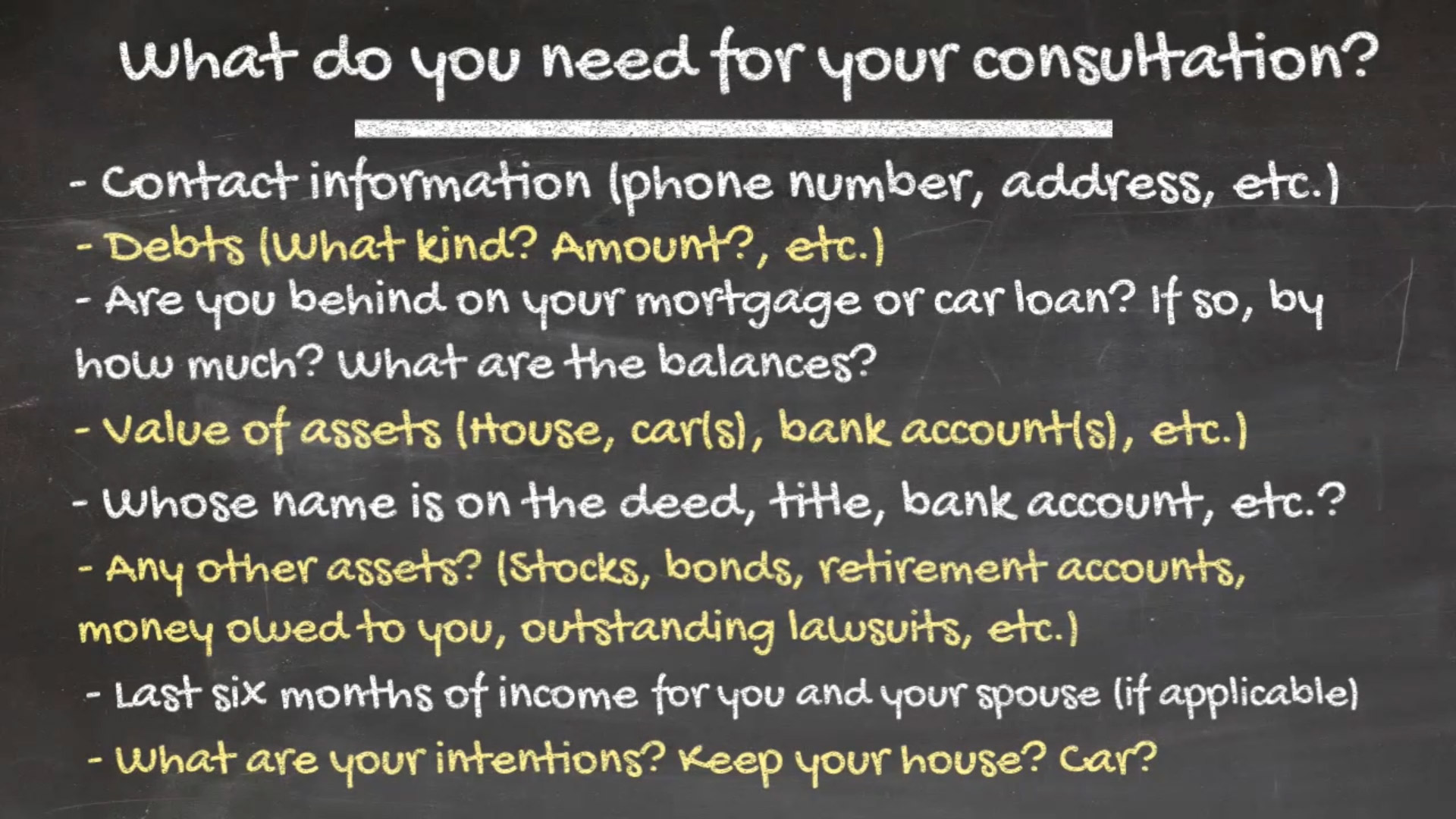

When you contact our office to speak to someone about bankruptcy, we normally schedule your free bankruptcy consultation first. Having as much information at the time of the consultation will ensure you get the best advice possible so we can start you on the process. We generally need the following information.

Contact Information

First, contact information. We will need the best contact information, such as phone and email address as well as the best mailing address for you. Throughout the process, we will need to send you documents and making sure they reach you in a timely manner, is important. If we can not contact you quickly and easily, we can not represent you.

Debts

During your free bankruptcy consultation, you will also need to have an estimate as to your debts, both unsecured and secured.

Examples of unsecured debts are:

- Credit cards

- Personal Loans

- Medical Bills

- Overdue Utilities

- Repossessed Cars

- Back Rent

Examples of secured debts are:

- Mortgages

- Home Equity Loans or Home Equity Lines of Credit

- Car Loans (even if you are the co-signer and it’s not ‘your car)

- Title Loans

If you are unsure of your total debt, we recommend you open a free Credit Karma Account.

Credit Karma pulls their information from two of the three credit reporting bureaus and gives you a solid idea of your outstanding debt. Often, items like medical bills and utilities will not be listed. It will become very important further into the process to be certain you have everyone you owe money to listed, but at this point, an estimate is fine.

You will also need to have information about your secured debts. We will need to know if you are current on your mortgage and/or car loan. If you are behind, how high are the arrears? What is the total balance on the loan? In addition to information about the loans, we will need to know approximately how much your house and car are worth. A quick look at Zillow or Kelley Blue Book will give you that information.

Assets

We will need to know about your assets. This includes everything from real estate you may own down to the pennies you may have in the couch cushions. No asset is to large or to small. Don’t worry though. Listing the assets does not mean that you will lose the asset. We can normally protect everything from the trustee – we just need to know about it.

Being certain you know who owns the assets as well will be imperative. With titled assets such as a house or car, the Deed or registration should give you that information. If you do not have the deed, or are unsure as to who is listed on the deed, you can easily obtain that information from your county’s Recorder of Deeds or Tax Assessment Office. The tax assessment office generally has an easy search feature that allows you to search for property addresses to determine owners.

We will also need information on your other assets. Do you have stocks or bonds? Outstanding lawsuit settlements? Money in any account? Retirement vehicles or life insurance? This initial consultation will help our office evaluate if we will be able to protect your assets. Knowing all of your assets will help get you the best advice.

Income

The bankruptcy court requires that the last six months of any and all income be disclosed and filed with the court. That means we will need the last six months of any and all pay stubs or a six-month profit and loss statement. At the time of the consultation, it is important that you know your gross income over the last six months.

Even if your spouse is not filing bankruptcy with you, if you are married and share a household, you MUST provide their income information as well. How much you make goes a long way toward our office’s recommendation on what bankruptcy chapter is best for you. If your estimate is off, due to overtime or incorrectly calculated income, when we get into the process, you may have issues filing the bankruptcy we had initially recommended for you. Having the correct information at the start means you get the best advice.

Household Size

The size of your household is important. There are several hurdles to jump through when evaluating your case for a Chapter 7 bankruptcy. One such hurdle is the means test. The means test looks at your income over a six-month period and compares it to the median income for a family of your household size, in the county you live. If you make more than that median income amount, you may not qualify for a Chapter 7 bankruptcy.

Your household is made up of you and anyone in your household you support. This could be a spouse or fiancé, children, grandchildren, or other relatives.

Intentions as to Secured Property and Leases

Knowing what you would like to do with your assets is crucial. If you are behind on your mortgage, do you want to keep the house? Are you just looking to buy time in the house and then sell it or surrender it back to the bank? Knowing what you are looking to do will again, help our office lead you in the right direction.