Curious about the Chapter 7 bankruptcy process? We have answers!

Chapter 7 bankruptcy is also known as liquidation. A Chapter 7 bankruptcy will allow you to get rid of all of your dischargeable debt within a matter of months, including credit card debt and medical bills. Chapter 7 bankruptcy is the most common chapter because it allows you to discharge your debt without making any payments.

While unsecured debt is discharged in a Chapter 7 bankruptcy, secured creditors retain their liens. In other words, if you have secured debt such as a mortgage, you still need to pay it to keep the property. If you don’t want to keep the property though, you will not have to pay. This is also the case for car loans.

In order to qualify for a Chapter 7 bankruptcy, your income must be below a certain level. That amount changes based on how many people you have in your house and what county you live in. It may also depend on certain payments you must make such as mortgage payments, car payments, and tax payments. If your income falls below this level, you may be a good candidate for Chapter 7.

How does the Chapter 7 bankruptcy process work?

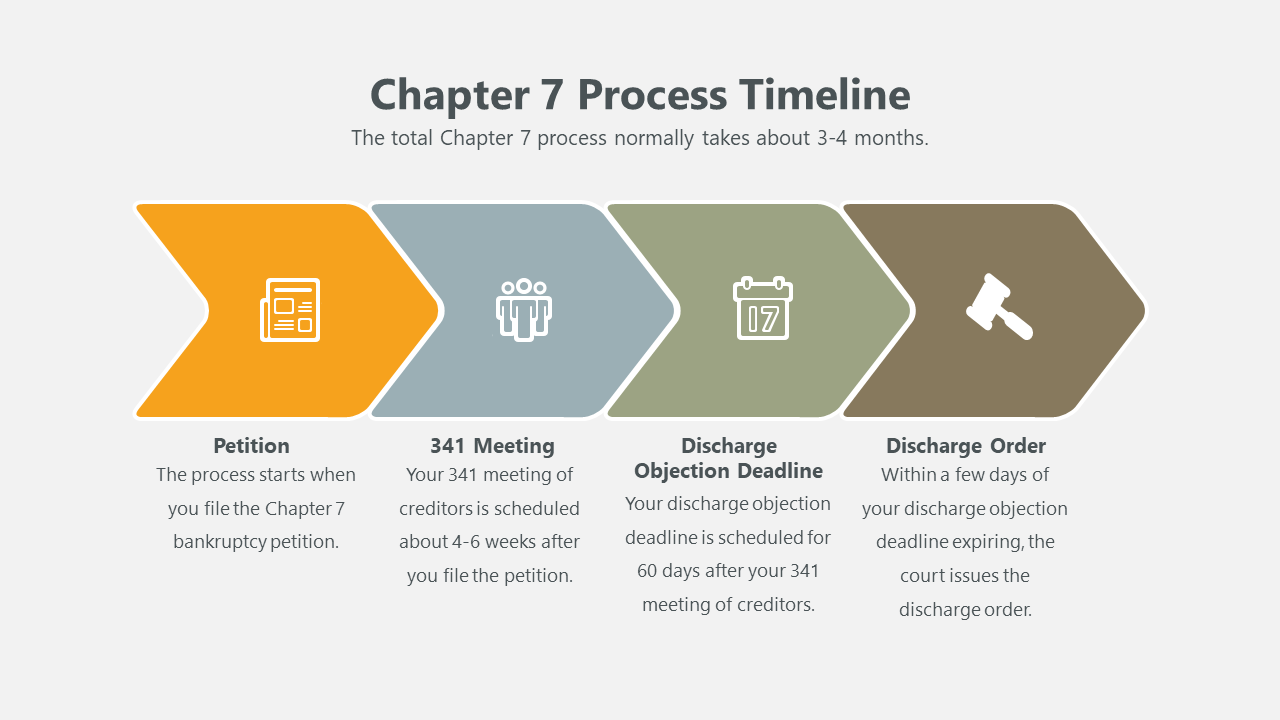

The concept of a Chapter 7 bankruptcy is simple. If you meet the income requirements, your debt is discharged (or forgiven) so long as a Chapter 7 trustee can sell your “non-exempt property” in order to pay some of your debt. In reality, very few people who file Chapter 7 bankruptcy have non-exempt property. To this vast majority of people, a Chapter 7 bankruptcy is merely a 3-4 month process after which they are free of unsecured debt. It is what people think of when they think “bankruptcy”. You file the Chapter 7 and a few months later you’re debt free.

The Chapter 7 341 Meeting of Creditors

In a Chapter 7 bankruptcy, a Chapter 7 trustee will be appointed to review your bankruptcy petitions and schedules. About 4-6 weeks after you file your Chapter 7 bankruptcy, you will have your 341 meeting of creditors. We discuss that meeting more thoroughly in our article “what happens at my Chapter 7 341 meeting of creditors?” It’s called a “meeting of creditors”, but creditors rarely show up at the meeting. It’s normally just you, your Chapter 7 bankruptcy attorney, and the Chapter 7 trustee.

Exempt vs. Non-Exempt Assets

The trustee will use this meeting to determine if you have “non-exempt assets”. In a Chapter 7 bankruptcy, you are only allowed to keep “exempt assets”. Each state has their own laws establishing what property is considered “exempt” property. Some states, such as Pennsylvania, New Jersey, and New York, allow you to choose between state-specific exemptions and “federal bankruptcy exemptions”. Other states, such as Maryland, require you to use state-specific exemptions.

The vast majority of Chapter 7 bankruptcy cases are “no asset” cases. This means that the trustee did not find any non-exempt assets. That is because people typically don’t file Chapter 7 bankruptcy cases if they have assets that they don’t want to lose. A Chapter 7 bankruptcy lawyer can tell you ahead of time if you have any assets that are non-exempt so you can make the decision before you file the Chapter 7. If you’re concerned that you may have non-exempt assets, you can file a Chapter 13 bankruptcy instead.

Can I keep my house in Chapter 7 bankruptcy?

In most cases, you are able to keep your house in a Chapter 7 bankruptcy, but you should consult a Chapter 7 bankruptcy lawyer to determine whether that is true in your case. Most states have rather large exemptions available for your primary residence. If you have a mortgage or other liens against your house, those would also reduce the home’s equity. In other words, if you have a $150,000 house with a $140,000 mortgage balance, you only have $10,000 in equity. Most states would allow for much more equity than this. As always, consult a Chapter 7 bankruptcy lawyer to determine if that’s true in your case.

Can I keep my car in Chapter 7 bankruptcy?

In most cases, you are able to keep your car in a Chapter 7 bankruptcy, but you should consult a Chapter 7 bankruptcy lawyer to determine whether that is true in your case. Cars depreciate quickly so most cars with a car loan are actually upside down. That means that there is little or no equity in your car and you can normally exempt it. As always, consult a Chapter 7 bankruptcy lawyer to determine if that’s true in your case.

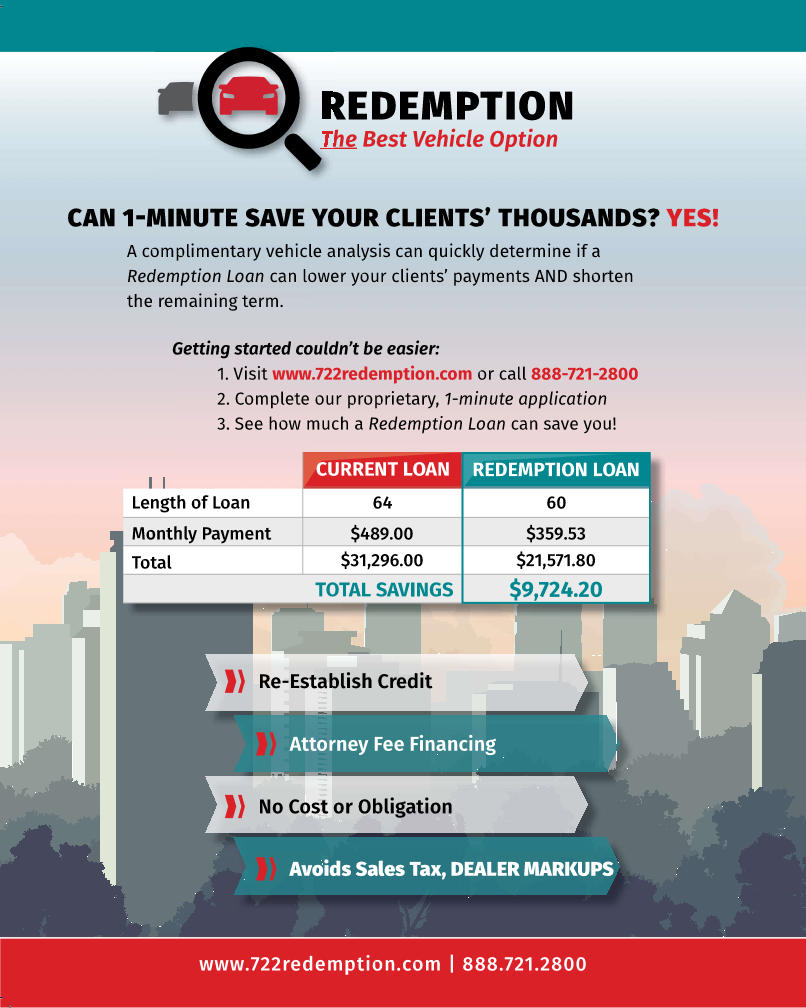

There’s also some magic available in Chapter 7 with regard to vehicles. If your car is worth less than the loan, you can potentially “redeem” the vehicle. That means you can keep it if you can pay the value of the car rather than the balance of the loan. Because cars depreciate so quickly, this can be very valuable. There are companies that offer “redemption loans” which act as a refinancing loan in most cases saving you significant money. It can also help you to re-establish credit.

If you don’t want to keep your current car, you can also get a “replacement loan”. This allows you to surrender your car and get a loan for a new one (or at least new to you). Yes, you can get a loan in bankruptcy. We have companies that we work with who specialize in these loans.

Can I keep my retirement account in Chapter 7 bankruptcy?

In most cases, you are able to keep your retirement account in a Chapter 7 bankruptcy, but you should consult a Chapter 7 bankruptcy lawyer to determine whether that is true in your case. The federal exemptions provide that qualified retirement accounts are fully exempt.

What happens after the 341 meeting of creditors?

After the meeting of creditors, the trustee, will file either a “Report of No Distribution” or a “Notice of Change to Asset Case”. If the trustee files a “Report of No Distribution”, it means that there is no non-exempt property for the trustee to liquidate. If the trustee files a “Notice of Change to Asset Case”, the trustee intends to liquidate some of your non-exempt property.

You will also need to take a second credit counseling course called a “Debtor Education Course” or “Financial Management Course”. You must file the certificate of completion to receive your discharge. We have more on that in our article “what happens after I file a Chapter 7 bankruptcy petition?”

When the 341 meeting is scheduled, the bankruptcy clerk will also schedule an objection deadline. This is the deadline for creditors or other parties to file an objection to discharge. This will be set 60 days after the first scheduled 341 meeting. If nobody objects, you should receive your discharge shortly thereafter.

Can my Chapter 7 bankruptcy be denied?

Not really. At least not in the sense people think of. It would not be your “bankruptcy” that is being denied. However, a Chapter 7 discharge may be denied in a few situations.

First, if your income is too high, the bankruptcy court can deny you a discharge in Chapter 7. This would mean you would need to convert to a Chapter 13 in order for your debts to be forgiven. This isn’t always bad though. Many of my clients actually pay less in a Chapter 13 than in a Chapter 7. How? A Chapter 13 is more powerful. You can do things in a Chapter 13 that you can’t do in a Chapter 7. For example, you may be able to “strip” a second mortgage in a Chapter 13 so that you don’t have to pay it.

Second, you may also be denied a discharge if you filed the bankruptcy in bad faith.

Third, certain types of debts may also be deemed “non-dischargeable”. That means those specific debts are not discharged and must be repaid. Typical non-dischargeable debts include student loans and certain taxes. (Yes, some taxes are dischargeable!) Learn more about the Chapter 7 discharge and non-dischargeable debts in our article here.

How long is the Chapter 7 bankruptcy process?

The Chapter 7 process from start to finish is normally about 3-4 months. From the time you file the bankruptcy petition, it is about 4-6 weeks for your 341 meeting of creditors. Your discharge objection deadline is set 60 days after that. You should receive your discharge shortly after your objection deadline passes. So all told, you’re looking at 3-4 months in most cases.

If the Chapter 7 trustee marks your case as an asset case or someone objects to your discharge, the case may take longer. Any unresolved issues will delay the closing of your bankruptcy case.

Can I change to Chapter 13 if I started as Chapter 7?

Generally, you can convert from a Chapter 7 bankruptcy to a Chapter 13 bankruptcy. However, the Chapter 7 to Chapter 13 conversion process requires you file a motion with the bankruptcy court and allow all creditors and parties in interest an opportunity to object. While you can generally convert from Chapter 7 to Chapter 13, you can be denied the opportunity to convert if you are found to have “bad faith conduct”.