Curious as to what happens after you file your Chapter 13 bankruptcy petition with our office? We have the answers!

Immediately after filing, you will receive an email or package from our office in the mail. Included with be several important pieces of information.

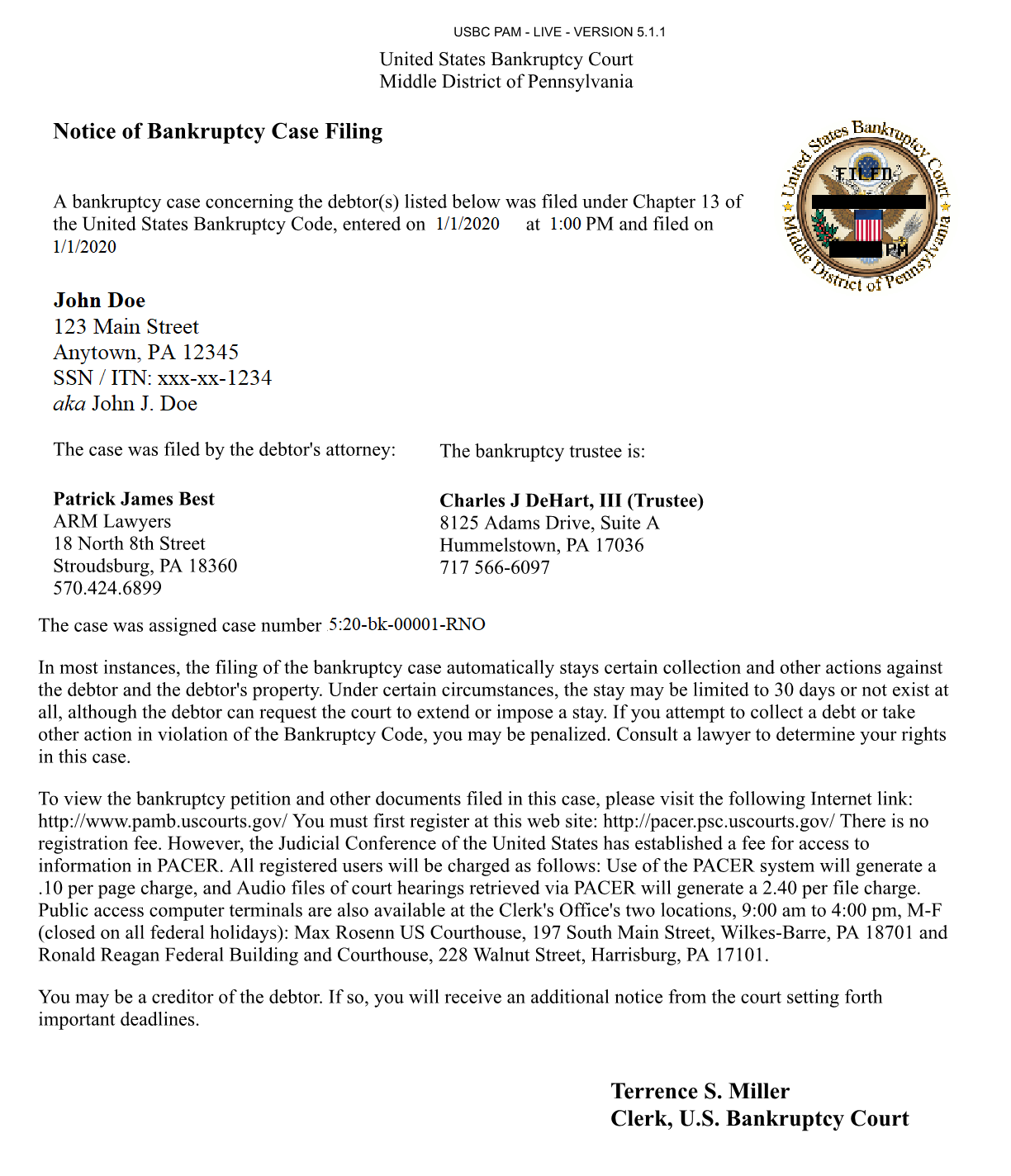

Notice of Bankruptcy Case Filing

Your Notice of Bankruptcy Case Filing is a vital and useful document that the court issues after we have filed your bankruptcy petition. In it, you will find your case number, district information as well as the date the petition was filed and often, your Trustee’s information. You can use this document to prove to anyone that you have filed bankruptcy and are under the protection of the Automatic Stay, which prohibits any creditors from contacting you or continuing with any collection actions.

Your case number will be important when you go to register for the second (and final) online credit course as well as when you register for the online payment program, which we discuss in more detail below.

Financial Management Course

The Financial Management Course is required by the court to be completed prior to the end of your bankruptcy. In most cases, your Chapter 13 bankruptcy will last anywhere from 3-5 years. Sounds like you have plenty of time, right? The issue is, if it is not completed and the certificate filed with the court before the end of your bankruptcy, you will not get your debt discharged. We recommend you take the course sooner rather than later.

Our Firm recommends BE Adviser for the post-filing course as they have fantastic customer service and a competitive rate. You will need to know you case number and district information, which is located on your Notice of Bankruptcy Case Filing.

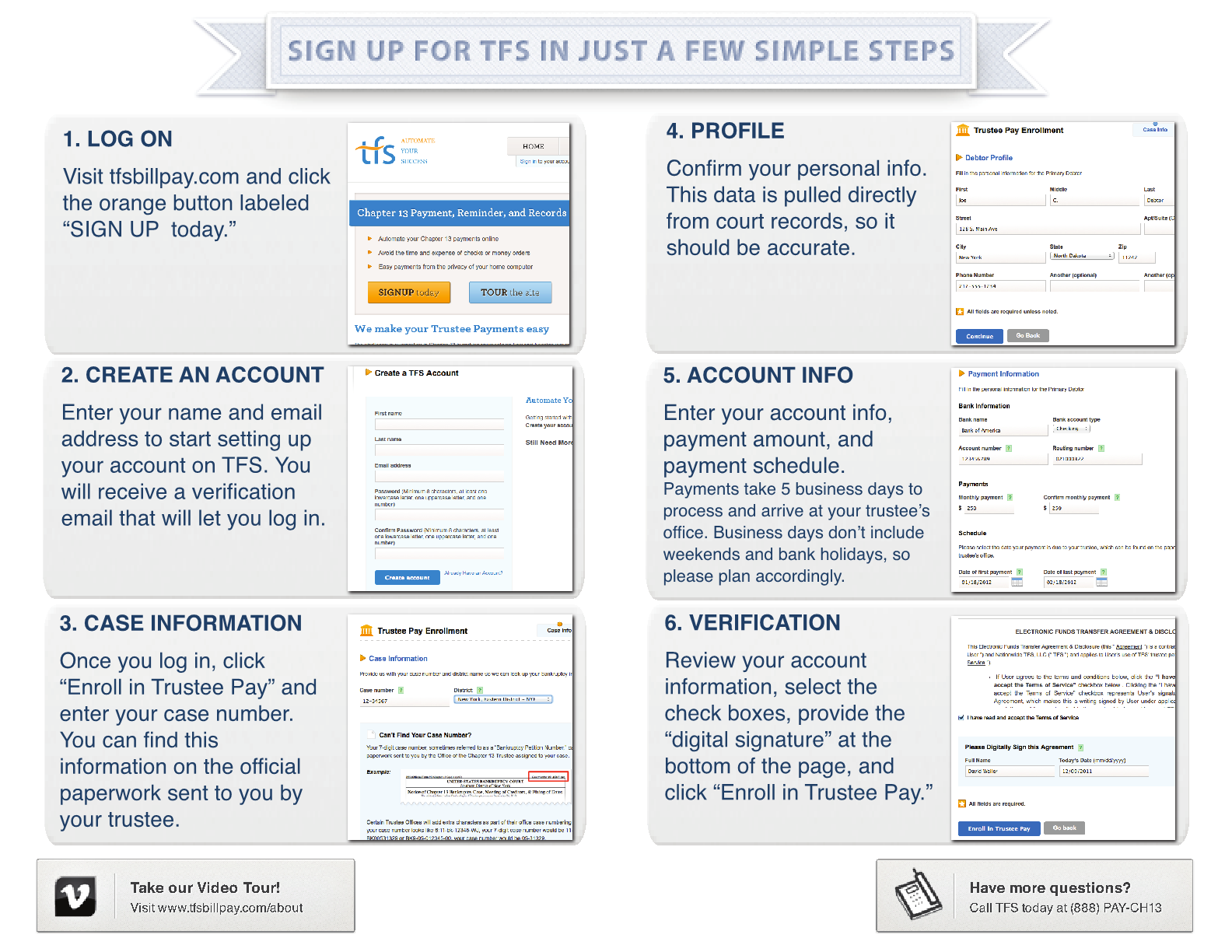

TFS Bill Pay

Your bankruptcy payment will become due the month after your bankruptcy is filed. The payment becomes due the first of the month, but as long as it is received prior to the end of the month it will be ‘on time’. If you fall behind by more than two months, your Trustee can and will file a Motion to Dismiss your case.

TFS Bill Pay is an online service that allows you to set up an account, enter your bank information and schedule recurring and one-time payments. Our office can log in and see pending payments or make sure your account has been suspended for deficient funds. The Trustee is also able to see pending payments, which can help us resolve any Motion’s to Dismiss if you do fall behind on payments.

Keeping our office updated if you fall behind on any payments to the bankruptcy court will help us make sure your bankruptcy stays viable.

Information on your Chapter 13 341 Meeting of Creditors

What happens at my Chapter 13 341 meeting? You will receive an email or letter from our office with information on your 341 Meeting of Creditors, including the location, date and time. In most cases, this meeting will be the one and only court date you will need to attend. At this meeting, your Trustee will verify your identity by using your Driver’s License and Social Security Card. If you do not have your Social Security Card, the Trustee will accept a W2 or 1099 as proof, but you are able to request a duplicate Social Security card online if you do not have your original copy. You MUST have both your Driver’s License and Social Security Card with you when you come to the 341 Meeting or the Trustee will not hold the meeting.

The 341 Meeting of Creditors is an opportunity for the Trustee to review any questions he may have about your bankruptcy petition as well as your proposed Chapter 13 Plan. Someone from our office will attend the meeting with you. There should be no questions you will not have answers to. The Trustee is just going to make sure someone from our office reviewed the petition with you, you have disclosed all of your assets and debts and you are who you say you are.

What documents does the trustee need for my meeting of creditors?

Each Trustee has different required documents they will request in advance of your 341 Meeting. No matter your Trustee, they all will require your most recently filed Federal Tax Returns. Our office should already have a copy, but if not, we will need them as soon as possible so we can get the documents to the Trustee prior to the meeting. If you do not submit the documents at least 7 days before the scheduled meeting, the Trustee will reschedule. Our office will let you know what specific documents your Trustee requires in that initial email or letter you receive after filing.

Keeping up with Payments

In some cases, your mortgage or car payment may be paid through your bankruptcy payment. If so, it is important that you make your full and complete bankruptcy payment on the first of the month. If the Trustee is sending your mortgage payment to the lender, he will not process that payment to the lender until the FULL payment is made. Your mortgage payment will be late if you are making your bankruptcy payment toward the end of the month.

If you are making your payment directly to your mortgage company or car finance company, you MUST make sure they payments are being received on time. Should you fall behind on any payments, the creditors can request permission from the court to start the foreclosure or repossession process. If you fall behind on any payments, either the bankruptcy payment or any payments you are making outside of the bankruptcy, you MUST let our office know.

How does Chapter 13 bankruptcy affect my credit score?

We’ve covered this topic in more detail in our article “what does bankruptcy do to my credit score?“. More often than not, debtors report an INCREASE in their credit score after filing for bankruptcy. How can this be possible? At ARM Lawyers, we do more than simply help you eliminate your debt. We will work with you to rebuild your credit score after bankruptcy! After your Chapter 13 Plan is confirmed, we will enroll you in the “7 Steps to a 720 Credit Score” program FOR FREE. This $1,000 program is available to my clients FOR FREE – just for being my client.

Protecting your assets

You must let our office know if anything happens to any of your assets. For example, if you are paying a car loan within your bankruptcy plan and you get in an accident, it may impact your bankruptcy plan payments.

Should you decide you want to sell your home while you are in bankruptcy, you must contact our office first. There are several steps and processes that must happen before you are able to sell your house while you are in bankruptcy, but it can be done.