A Chapter 7 bankruptcy discharge is a very powerful thing. It stops your creditors from pursuing discharged debts permanently. But it can also be confusing. Let’s answer some of the common questions about the Chapter 7 discharge.

What does a Chapter 7 discharge mean?

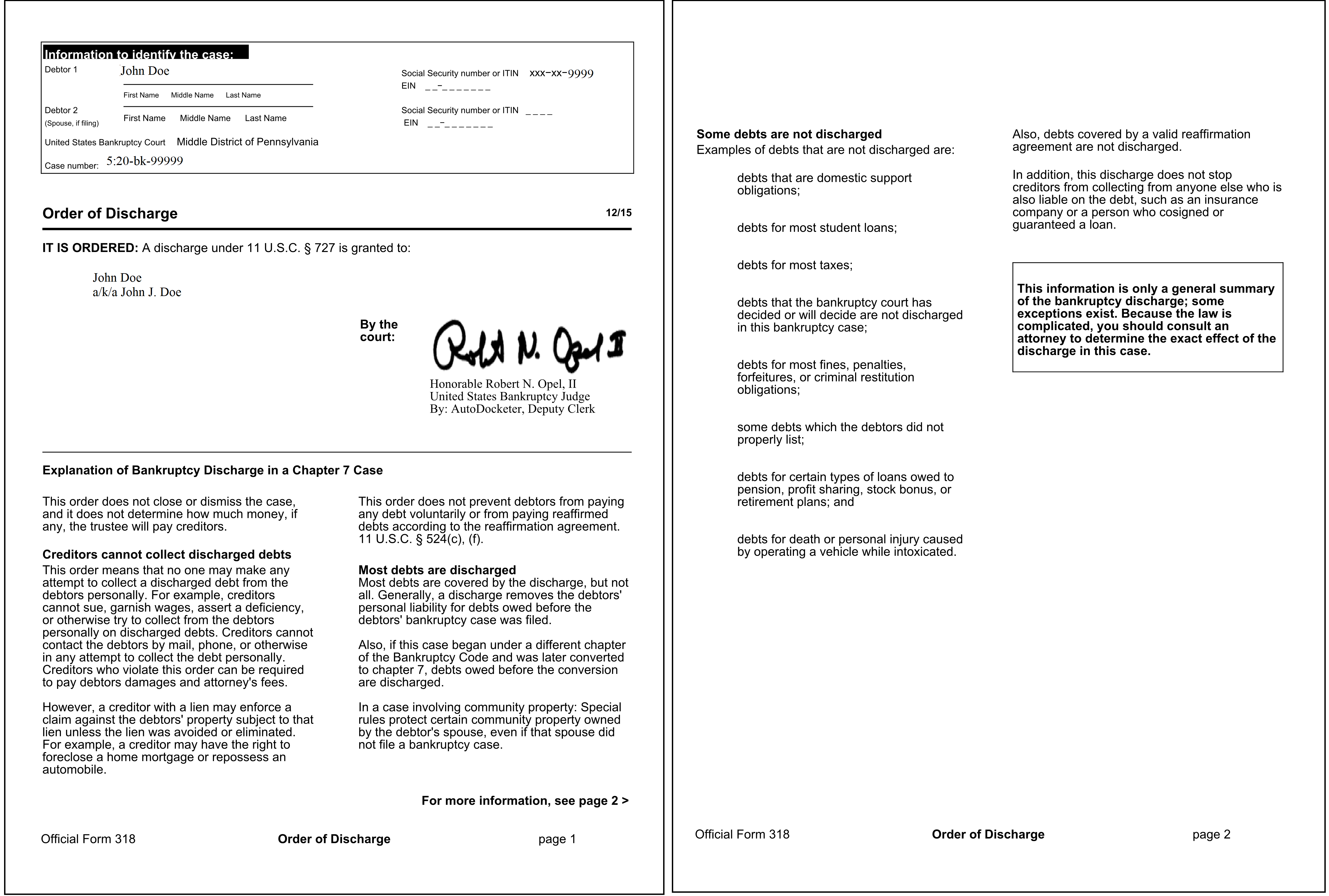

A “discharge” is the fancy legal term for your debts being forgiven in your bankruptcy. When we talk about debts forgiven in bankruptcy, we would say that your debts are discharged. The Chapter 7 “discharge order” is the final order you receive in your Chapter 7 bankruptcy. It is signed by the bankruptcy judge assigned to your cases and states clearly that you have received a Chapter 7 discharge. In other words, it is the formal document that releases you of your debts.Some people refer to the order less formally such as “discharge papers”.

What does my Chapter 7 discharge order look like?

While every court is slightly different, the Chapter 7 discharge order looks similar. It is signed by a judge and states that “A discharge under 11 U.S.C. § 727 is granted to: Your Name”.

What is a Chapter 7 discharge injunction?

Once you get your discharge, your creditors are “enjoined” from pursuing the debt. That means that the court has ordered them to stop collection activity. If your creditors ignore this order, you may be able to get damages caused by their actions. We typically see this in cases where debt collection companies continue to send payment demands even though the person received the discharge. In these cases, we have sued the debt collectors and won. The discharge is serious and debt collectors should respect it.

Is debt discharged in a Chapter 7 taxable?

No! One of the greatest things about bankruptcy is that your debt is discharged tax free. If you were to settle your debt with your debt collectors, you would receive a 1099 at the end of the year. You would have to pay tax on any money forgiven by the debt collector. In bankruptcy, the discharge makes it so that the debt forgiveness is not taxable.

I got a 1099 from my creditor even though my debt was discharged in bankruptcy. What do I do?

This happens. It’s an accounting issue for the creditor. No worries though. You can simply complete an IRS Form 982 when you complete your tax returns to explain you have a bankruptcy discharge. If you file this form, you won’t have to pay tax. If we file your taxes for you, we will do this for you so you don’t have to worry about it.

When will I get my discharge?

We discuss the timeline in the Chapter 7 bankruptcy process, but generally, you will receive the discharge order about 3-4 months after you file your bankruptcy petition in most cases. The deadline to object to the discharge is 60 days after your first scheduled 341 meeting of creditors. After that deadline expires, the court will normally issue the discharge order in a day or two.

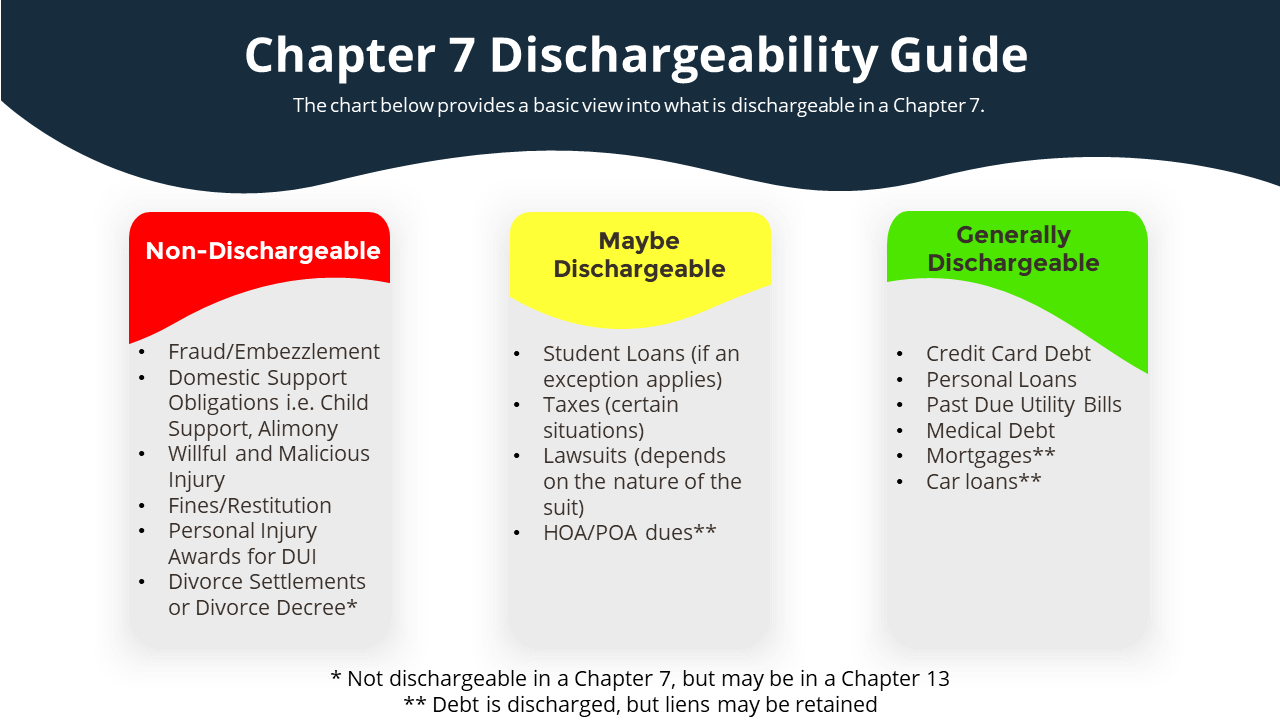

What debts are dischargeable in a Chapter 7 bankruptcy?

Most debts are dischargeable in Chapter 7 with a few exceptions. So we generally start by assuming the debt is dischargeable unless an exception applies. The common exceptions to dischargeability are:

- Fraud/Embezzlement

- Domestic Support Obligations i.e. Child Support, Alimony

- Willful and Malicious Injury

- Fines/Criminal Restitution

- Personal Injury Awards related to a DUI

- Divorce Settlements or Divorce Decree (not dischargeable in Chapter 7, but may be dischargeable in Chapter 13 bankruptcy)

- Some Homeowner’s Association (HOA) or Property Owner’s Association (POA) dues (the rules on this are complex)

- Some taxes (the rules on this are complex)

- Student loans (unless an exception applies)

As you can see, some types of debt are not black and white. Notably, taxes and homeowner’s association dues have complex dischargeability rules. In fact, tax dischargeability is so complicated, we perform a full tax dischargeability analysis for our clients. Many times these debts are dischargeable. You should speak with a Chapter 7 bankruptcy attorney to see if they are dischargeable in your case.

Can a Chapter 7 discharge tax debt?

Yes, in some cases. The tax dischargeability rules are very complex. Generally, we can discharge income taxes due more than three years ago provided that the returns were filed more than two years ago. Additionally, liens are retained in a Chapter 7 so even if the debt is discharged, the IRS would retain its lien until it expired.

However, we know the ins and outs of tax dischargeability – not only from the bankruptcy side, but also from the tax resolution side. When we have a client with tax issues, we first perform a full tax dischargeability analysis. We determine which tax debts are dischargeable and which tax debts are not. We would then develop a strategy for dealing with the non-dischargeable tax debts. Sometimes, we can use an Offer in Compromise or a financial hardship plan. Other times, we simply need to have get your federal tax lien released.

Can a Chapter 7 discharge student loans?

Yes, in some cases, you can discharge student loans in Chapter 7 bankruptcy. A common misconception, amongst both student loan borrowers and attorneys, is that student loans cannot be discharged in bankruptcy. This is absolutely not true. Both federal and private student loans can be discharged in bankruptcy.

To be clear, the default rule is that student loans are not dischargeable, but there are exceptions to this rule. Although this can be difficult, we have the experience and knowledge to craft arguments that best fit your situation.

Generally, if we’re trying to discharge student loans in bankruptcy, we would use one of the following exceptions to the rule:

- Undue Hardship: The standard for discharging student loans through bankruptcy is that the debt will impose an undue hardship on you and your dependents. The test used by most courts is known as the Brunner test and this test looks at three factors that are generally very subjective.

- Non-Qualified Educational Loan: The Bankruptcy Code requires private student loans to be “educational loans”, which differ from other types of consumer debts, and be incurred solely for higher education expenses.

- Eligible Student: An additional requirement for a qualified educational loan is that the private student loan borrower is an eligible student during the period of the loan. Some factors of an eligible student include being a US citizen or eligible non-citizen and enrollment in an eligible degree.

- Eligible Institution: The college or university at which a private student loan borrower is enrolled must be an eligible institution. It is important to look for institutions that are unaccredited.

Additionally, we have seen great success with dealing directly with the Department of Education’s Administrative Discharge Application. In most cases, this is a cheaper and better option. For example, if you are permanently disabled, you would likely qualify for an administrative discharge more easily than a bankruptcy discharge.

If student loans are a concern for you, you should speak with a student loan lawyer in our office. That way we can address your specific situation to determine if your student loans are dischargeable.

Can a Chapter 7 discharge child support?

No. Child support cannot be discharged. However, if you are simply seeking relief from collection on child support arrears, a Chapter 13 bankruptcy can provide for a comfortable repayment plan. The arrears must be paid in Chapter 13, but you would have up to five years to repay them and in the meantime, collection activity would be stopped.

Can a Chapter 7 discharge divorce settlements?

No, divorce settlements are not dischargeable in Chapter 7. However, divorce settlements and divorce awards may be dischargeable in Chapter 13 bankruptcy. In fact, we’ve had clients choose to file a Chapter 13 bankrutpcy for this reason. If you have a large divorce debt, it may justify filing a Chapter 13 rather than a Chapter 7 so that this debt becomes dischargeable.

Does a Chapter 7 remove negative items from my credit report?

Yes! One of the best parts about Chapter 7 bankruptcy is that negative items are removed from your credit report. This allows you to build credit quickly after bankruptcy. We’ve discussed this in our article “what does bankruptcy do to my credit?” Many times, your credit report begins to show these items as removed within a month or two of filing bankruptcy. This causes many of our clients to see their credit score go up as much as 50 points after filing a bankruptcy!

Will a Chapter 7 discharge remove a foreclosure from my credit report?

Yes! A Chapter 7 will remove any negative items regarding your foreclosure. It will remove the indication of the foreclosure itself, but also the missed payments leading up to the foreclosure. The Chapter 7 will also prevent you from being sued for a “deficiency judgment” and will prevent you from being taxed on any deficiency that is forgiven.

Will a Chapter 7 discharge remove a vehicle repossession from my credit report?

Yes! A Chapter 7 will remove any negative items regarding your repossession. It will remove the indication of the repossession itself, but also the missed payments leading up to the repossession. The Chapter 7 will also prevent you from being sued for a “deficiency judgment” and will prevent you from being taxed on any deficiency that is forgiven.

Moreover, a Chapter 7 can help you get a new car loan! It’s unbelievable to a lot of my clients, but we see people get car loans the day we file a Chapter 7.

Will a Chapter 7 discharge remove a judgment from my credit report?

Yes! A Chapter 7 removes judgments from your credit report. If you are subject to a judgment lien, you may need to file a Motion to Avoid Lien in order to remove it completely. Your Chapter 7 bankruptcy attorney can discuss this with you and determine if you qualify for lien avoidance.

What happens to liens in a Chapter 7?

The general rule is that liens are retained in Chapter 7. That means if you have a consensual lien such as a mortgage or a car loan, the lien stays attached to the property. There are exceptions though. You may redeem your vehicle, for example. This allows you to remove the lien.

What happens to my mortgage in Chapter 7?

The fact that the lien stays attached to the property leads us in an interesting position. Technically, you no longer owe the debt. The bank can never sue you for defaulting on your mortgage. On the other hand, if you want to keep the house, you will need to pay the mortgage. If you don’t pay the mortgage, the bank can still foreclose even though the debt is discharged.

If you wanted to walk away from the house without paying the mortgage, you can. Since the debt is discharged, you will never be sued for a deficiency judgment. The bank will foreclose on the home, but will not ask you to pay.

What happens to my car loan in Chapter 7?

Much like with mortgages, the fact that the lien stays attached to the property leads us in an interesting position. Technically, you no longer owe the debt. The bank can never sue you for defaulting on your car loan. On the other hand, if you want to keep the car, you will need to pay the loan. If you don’t pay the car loan, the bank can still repossess it even though the debt is discharged.

That being said, there’s also some magic available in Chapter 7 with regard to vehicles. You can “redeem” the car if your car is worth less than the loan. That means you can keep it if you can pay the value of the car rather than the balance of the loan. Because cars depreciate so quickly, this can be very valuable. There are companies that offer “redemption loans” which act as a refinancing loan in most cases saving you significant money. It can also help you to re-establish credit.

If you don’t want to keep your current car, you can also get a “replacement loan”. This allows you to surrender your car and get a loan for a new one (or at least new to you). Yes, you can get a loan in bankruptcy. We have companies that we work with who specialize in these loans.

What happens to tax liens in Chapter 7?

Tax liens survive Chapter 7. If the tax debt was dischargeable, the IRS will never try to collect on the debt, but the lien will stay attached to your property.

If you have a tax lien, pre-bankruptcy planning becomes invaluable. We can employ some advanced strategies to remove the liens prior to filing the bankruptcy. You can then file your bankruptcy and have the tax debt discharged.

Tax debts in bankruptcy are complex. Most bankruptcy attorneys do not even understand them. Since we are also tax resolution attorneys, we deal with the IRS all the time. If you have a tax issue, we will have a discussion about your tax debt prior to filing the bankruptcy.

Can my Chapter 7 bankruptcy be denied?

Not really. At least not in the sense people think of. It would not be your “bankruptcy” that is being denied. However, a Chapter 7 discharge may be denied in a few situations.

First, if your income is too high, the bankruptcy court can deny you a discharge in Chapter 7. This would mean you would need to convert to a Chapter 13 in order for your debts to be forgiven. This isn’t always bad though. Many of my clients actually pay less in a Chapter 13 than in a Chapter 7. How? A Chapter 13 is more powerful. You can do things in a Chapter 13 that you can’t do in a Chapter 7. For example, you may be able to “strip” a second mortgage in a Chapter 13 so that you don’t have to pay it.

Second, you may also be denied a discharge if you filed the bankruptcy in bad faith.

Third, certain types of debts may also be deemed “non-dischargeable”. That means those specific debts are not discharged and must be repaid.