Time to go head to head: bankruptcy vs. debt consolidation. Debt consolidation and debt settlement are related, but distinct, ways to deal with debt. People tend to explore debt consolidation or debt settlement prior to considering bankruptcy. We get asked questions comparing bankruptcy to debt settlement or debt consolidation all the time: Bankruptcy or debt settlement? Bankruptcy or debt consolidation? Here we’ll breakdown common myths and misconceptions that show you the pros and cons of bankruptcy versus debt settlement.

First, let’s explain the differences between debt settlement and debt consolidation. In debt settlement, you are typically paying a company to settle your debt for less than the total amount you owe. In debt consolidation, you are typically paying a company to manage your debt payments to third party creditors. This allows you to pay one company versus paying several.

To the untrained eye, both sound like reasonable options until you realize the problems. In most cases, you end up in a far worse position than if you had simply filed a bankruptcy.

Both debt consolidation and debt settlement come with a number of issues.

Issues with Debt Consolidation and Debt Settlement

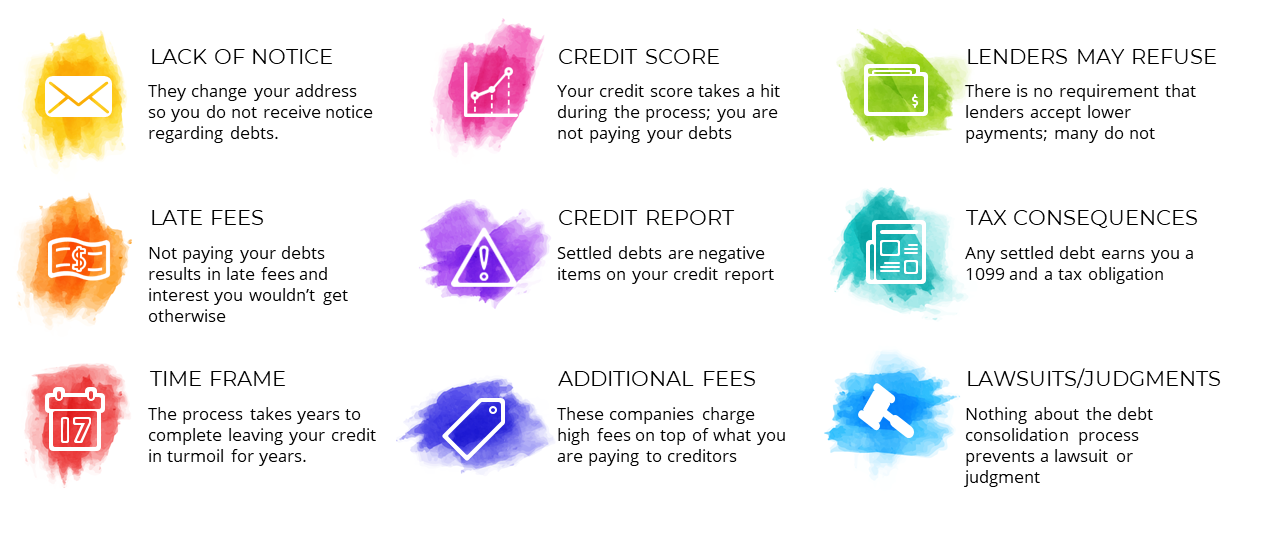

- Lack of notice – These companies often change your address so you do not receive notice regarding your debts. This can lead to you being in the dark throughout the process.

- Late fees – In order to try to settle your debt, these companies will tell you to stop paying your credit cards. This results in late fees being applied to your account. In many cases, you’ll pay more money than you would have otherwise.

- Time frame – The process in debt consolidation or debt settlement can take years. The entire time, your credit is in turmoil and your life remains upside down.

- Credit score – When you stop paying your debts, the late payments are reported on your credit report. If you thought you were saving your credit by avoiding bankruptcy, you are not. The damage to your credit is often worse in debt settlement. We’ll explain more below.

- Credit report – Debt settlements themselves are “derogatory remarks” on your credit report. The debt is marked as “settled” on your report and that damage will remain for seven years. Yuck.

- Additional fees – The debt consolidation or debt settlement companies often charge so much money that most of the payments you make goes to them rather than your debt.

- Lenders may refuse – Just because you want to settle your debt, doesn’t mean you can. The lender still has to agree. Often times, they won’t. Several lenders have a non-negotiable policy of non-settlement. They would rather accept $0 than settle with you. This is surprising to people.

- Tax consequences – Debt settlement results in a 1099 and taxable income for any amount forgiven. There goes your refund next year.

- Lawsuits/Judgments – During the debt settlement process, you will likely be sued. Many times a judgment will be entered against you. Nothing about the debt settlement process protects you from this.

Bankruptcy on the other hand, provides a number of protections for you.

Benefits of Bankruptcy

- Notice Throughout – You will know everything that happens in your case from start to finish. No surprises.

- No Late Fees – Even if you stop paying your credit card payments, you will not have to pay any late fees since in most cases you are not repaying any debt.

- Time Frame – A Chapter 7 bankruptcy takes about 3-4 months to complete. Stark contrast to the years that debt settlement can take.

- Credit Score – Contrary to popular belief, bankruptcy can improve your credit score. Most of my clients report an immediate increase of about 50 points.

- Credit Report – It is easier to repair your credit after a bankruptcy than after debt settlement. The reason is simple. A bankruptcy is one singular derogatory remark. In debt settlement, you earn multiple derogatory remarks in addition to late payments. Those remarks stay on your credit report for years. Bankruptcy debtors rebound from bankruptcy quickly. My clients can get a car loan the day they file bankruptcy in most cases!

- Flat Fees – Bankruptcy fees are typically “flat fees” meaning that there is a singular price quoted up front. No hourly billing. No surprises. One low fee quoted at the beginning. Plus, it’s always lower than debt settlement fees by a large margin.

- Lenders Can’t Refuse – They may want to, but they can’t. As long as you’re not perpetrating a fraud, there’s not much they can do.

- No Tax Consequences – None. Zero. Debt discharged in bankruptcy is tax free.

- Lawsuits/Judgments – Complete and total protection. All lawsuits are stayed by the bankruptcy.

Chapter 7 qualification often requires qualification under the means test. As such, you can use the free Chapter 7 calculator below to estimate qualification and get a free bankruptcy consultation.

Is debt settlement better than bankruptcy?

The short answer is no. It’s almost always worse for you. We actually discuss the credit impact of bankruptcy in more depth in our article “what does bankruptcy do to my credit?”

While it sounds great to settle your debt for pennies on the dollar it rarely works out that way. More often than not, debt settlement companies charge you large amounts of money to get no results. There are a number of lenders that will not negotiate with you regardless of what any debt settlement company tells you.

Many times people seek this option to avoid negative credit score impacts. Unfortunately, your credit will almost always suffer more from debt settlement than from bankruptcy. Debt settlement results in more negative items and late payments. Bankruptcy removes those items and leaves only the bankruptcy itself behind. Bankruptcy also offers a far quicker credit rebound.

Additionally, you’ll likely have to deal with being sued while in debt settlement.

I have too many clients that came from unhappy debt settlement programs only to file bankruptcy anyway. Why not start there and avoid the hassle and save yourself some money? When considering bankruptcy vs. debt settlement, bankruptcy wins in just about every case.

If you’re concerned about the credit impact, don’t be. We do more than simply help you eliminate your debt. We will work with you to rebuild your credit score after bankruptcy!

Is debt consolidation better than bankruptcy?

Also, no. Even if your goal was to repay your debt, you can always do that at better terms in bankruptcy. In a Chapter 13 bankruptcy, we can lower car interest rates and even principal payments if you qualify. We can have you repay your debts at 0% interest. It’s nearly impossible to get better terms in a debt consolidation program and it is almost always more damaging to your credit score. When considering bankruptcy vs. debt consolidation, bankruptcy wins in just about every case.

So what’s better? Bankruptcy vs. Debt Consolidation

If you’re considering debt settlement or debt consolidation, you owe it to yourself to consider bankruptcy. Don’t end up like my clients who throw away tens of thousands of dollars to debt consolidation before filing bankruptcy. Bankruptcy vs. debt consolidation? No contest. Call us now so we can review your situation with you and see if bankruptcy is right for you.